Differences between the Polish Accounting Act and International Accounting Standards (IAS)

The ongoing process of adjusting Polish legislation to international accounting regulations has been carried out for years. It can be also observed that both national and international provisions are subject to constant changes. Nevertheless, there are still differences between those regulations, which cause that relevant values are differently presented in financial statements.

The growing globalisation of investments and raising capital cause that investors are increasingly interested in foreign investments. These processes constitute and will constitute the key factor stimulating works on uniform accounting standards. Introducing by individual countries uniform accounting approach would significantly facilitate foreign investments and the preparation of financial statements, involving lower costs1.

The basic legal act regulating accounting rules which concern business entities in Poland is the Accounting Act of 29 September 1994, consolidated text. Journal of Laws of 2013, item 330 (last amendment: Journal of Laws of 2015, item 1893).

Article 1. Scope of the regulation The Act specifies accounting principles, procedures for the audit of financial statements by statutory auditors and principles for conducting activity with regard to bookkeeping services.

Article 2. Application of the provisions of the Act 1. The provisions of the Accounting Act, hereinafter referred to as “the Act”, are applied, subject to the provisions of Paragraph 3, to the following entities whose registered offices or place of executive management are located on the territory of the Republic of Poland:

- commercial companies (partnerships and capital companies, including organisations), and civil partnerships, subject to the provisions of point 2, as well as other legal entities, except for the State Treasury and the National Bank of Poland;

- natural persons, civil partnerships established by natural persons, general partnerships established by natural persons and professional partnerships, if their net revenue from sales of goods, products and financial transactions for the preceding financial year amounted to at least the PLN equivalent of EUR 1 200 0002.

Commercial law companies, natural persons generating revenues of at least EUR 1 200 000 translated into the Polish currency for the preceding financial year and other entities listed in Article 2 of the Act with their registered offices or place of executive management on the territory of the country prepare financial statements on the basis of the Act.

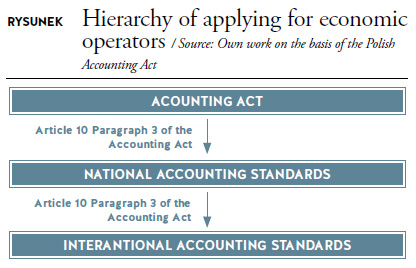

The hierarchy of provisions for business entities which apply the Accounting Act is established by:

Article 10. Paragraph 3. of the Accounting Act. In matters not provided for in the provisions of the Act, while adopting accounting principles (policy), entities may apply national accounting standards issued by the Accounting Standards Committee. If there is no applicable national standard, entities other than specified in Article 2 Paragraph 3 may apply IAS.

Article 45. Accounting Act Financial statements prepared pursuant to IAS

1a. Financial statements of issuers of securities admitted to, issuers of securities intending to file for admission to or issuers of securities pending admission to trading on one of the regulated markets of the European Economic Area countries may be prepared pursuant to IAS.

1b. Financial statements of entities being members of a capital group, in which a parent company prepares a consolidated financial statement pursuant to IAS, may be prepared pursuant to IAS.

1c. The decision in respect of the preparation of financial statements pursuant to IAS by the entities referred to in Paragraphs 1a and 1b, is taken by an approving body.

1d. The approving body may take the decision to discontinue the application of IAS for the preparation of financial statements by entities if the circumstances referred to in Paragraphs 1a and 1b cease to exist.

1e. Financial statements of branches of foreign companies may be prepared pursuant to IAS if this contractor prepares financial statements pursuant to IAS.

As entities’ statements may be prepared on the basis of the Accounting Act or pursuant to the rules of IAS, the table shows an overview of the differences.

Example

The LUXUS company on 6 December 2015 bought a production machine at the price of PLN 380 000.00. Annual amortisation rate 20%. Line amortisation method. After 5 years it intends to sell the machine for the amount of PLN 60 000.00.

Settlement of the operation:

- Pursuant to the Accounting Act

- Pursuant to the rules of IAS

Variant 1.The company prepares the financial statement pursuant to the Accounting Act.

It has been laid down in the company’s accounting policy that tangible assets are depreciated pursuant to the Polish Corporate Income Tax Act, i.e. from the month following the month in which the asset is brought into use.

Amortisation since January 2016

Every year

380 000.00 x 20% = PLN 76 000.00

Variant 2.The company prepares the financial statement pursuant to IAS

Amortisation since December 2015

We determine the basis

380 000.00 – 60 000.00 = PLN 320 000.00

In December 2015

320 000.00 x 20% = 64 000.00 / 12 = 5 333.33

Amortisation in the subsequent years in the amount of PLN 64 000.00

|

No. |

DESCRIPTION |

ACCOUNTING ACT / ACCOUNTING STANDARDS COMMITTEE |

IAS / IFRS |

|

1 |

Presentation of Financial Statements |

Article 45 of the Act |

IAS 1 |

|

Precise definition of a financial statement. Components:

|

The entity may use different names of appendices:

|

||

|

2 |

Stocks |

Article 34 of the Act |

IAS 2 |

|

Valuation Expenditure |

Entities may assess the value of materials and goods at the purchase price if it does not distort the value of assets, or on the basis of the acquisition price or manufacturing cost. The following methods can be applied: FIFO, LIFO, average weighted |

Only on the basis of the acquisition price or manufacturing cost Inapplicability of LIFO method (last in, first out) |

|

|

3 |

Classification and definitions of fixed assets |

Article 3 item 15 |

IAS 16 |

|

Components Commencement of amortisation Amortisation methods |

Conditions for including an asset into fixed assets:

Distinguished:

Not regarded as fixed assets Not earlier than after putting the fixed asset into operation, i.e. in the following month For example the progressive method – write-offs increase over the useful life Once established, amortisation methods are not changed. |

Fixed assets:

There is no requirement for completeness It does not contain such distinction, the application is voluntary Each component of tangible assets whose acquisition price or manufacturing cost is significant in relation to the acquisition price or manufacturing cost of the entire item is depreciated separately. When the item of tangible assets is available for use Method not allowed It specifies the verification at the end of each financial year and the possibility to introduce changes |

|

|

4 |

Intangible assets |

Article 3 point 14 |

IAS 38 |

|

Property rights acquired by the entity suitable for economic use, whose expected useful economic life exceeds one year, intended to be used for the entity's needs, in particular: author’s property rights, related rights, licences, concessions or other |

The period of use is specified or unspecified. Components with unspecified period of use are not subject to depreciation charges. An impairment test is carried out annually or if there is evidence that an impairment loss has been incurred |

||

|

5 |

Presentation of investment properties |

Article 3 point 17 |

IAS 40 |

|

Including into investments, and consequently into tangible assets |

Including into tangible assets, but it is also possible to include them into current assets |

EXERCISES

Task 1. Key phrases

Read the text carefully and study the vocabulary. Translate the selected key words from the text into English:

- trwający/w toku: ..........................................

- podlegać: ......................................................

- osoby fizyczne: .............................................

- zgodnie z: .....................................................

- zmniejszać się: ..............................................

- rachunek zysków i strat: ...............................

- środki trwałe: ................................................

- szacować: .......................................................

- wycena: ..........................................................

- stosowany: .....................................................

Task 2. Words in context

Use the words from task 1 in correct forms to complete the sentences below:

- In most countries, every year, taxpayers have to complete self-.......................................... tax returns which they next submit to local tax offices.

- The number of university students pursuing careers in state education .......................................... significantly in comparison to previous years.

- In case of tailor-made contracts, general terms of cooperation will no longer be .........................................., unless stated otherwise.

- At today’s .........................................., in our pawnshop, you are bound to get about 25 hundred dollars for the unique golden pendant you have brought.

- The entire process of production and assembly .......................................... a close scrutiny by a panel of experts before it was finally implemented in the factory in 1986.

- According to the opposition, the government has to solve all .......................................... problems concerning unemployment benefits long before it decides to impose new taxes.

- Native Indians in American reservations have always tried to maintain their tradition and culture by living .......................................... their inherited customs, the majority of which date back even to the 15th century.

- A certified accountant will be eager to help you with your corporate finances or cash-flow, especially with your monthly ..........................................

- Basic legal and financial advice for .......................................... intending to start their own businesses can be obtained for free in our local labour offices on weekdays, from 8 to 10 am.

- By definition, .......................................... have material or physical forms, and they include both fixed and current assets such as property, vehicles, machinery, stocks and cash.

Task 3. Comprehension check

Decide whether the sentences below are true (T) or false (F) according to the text:

- Both national and international rules of accounting are changing constantly. ................

- Uniform accounting guidelines are the result of market globalization in European countries. ................

- The Accounting Act of 1994 applies to business entities with registered offices outside Poland. ................

- Revenues for the preceding year generated by natural persons should always be expressed in total in the European currency. ................

- All financial reports of issuers or entities should be prepared in accordance with IAS. ................

- As stated in the IAS 1, it is allowed to use varied names of appendices in financial statements. ................

- In the IAS 16, fixed assets require completeness and they can no longer be used for 12 months. ................

- The acquisition price of a fixed asset is insignificant in relation to the manufacturing cost. ................

- According to the IAS 40, all stocks and investment properties can be included in current assets. ................

- Financial statements prepared by one company according to the Accounting Act or to the rules of IAS may vary considerably in terms of amortization. ................

KEY to exercises

Task 1

- Pending

- Be subject to

- Natural persons

- Pursuant to

- Decrease

- Profit and loss account

- Tangible assets

- Assess

- Valuation

- Applicable

Task 2

- Assessment

- Has decreased

- Applicable

- Valuation

- Was subject to

- Pending

- Pursuant to

- Profit and loss account

- Natural persons

- Tangible assets

Task 3

- T

- F

- F

- F

- T

- T

- F

- F

- F

- T

Przypisy / Źródła

- Bailey G.T., Wild K., Deloitte & Touche, Międzynarodowe Standardy Rachunkowości w praktyce, Accountancy Development Foundation in Poland, Warsaw 2000.

- Accounting Act of 29 September 1994 (Journal of Laws, no. 121, item 591 as amended).